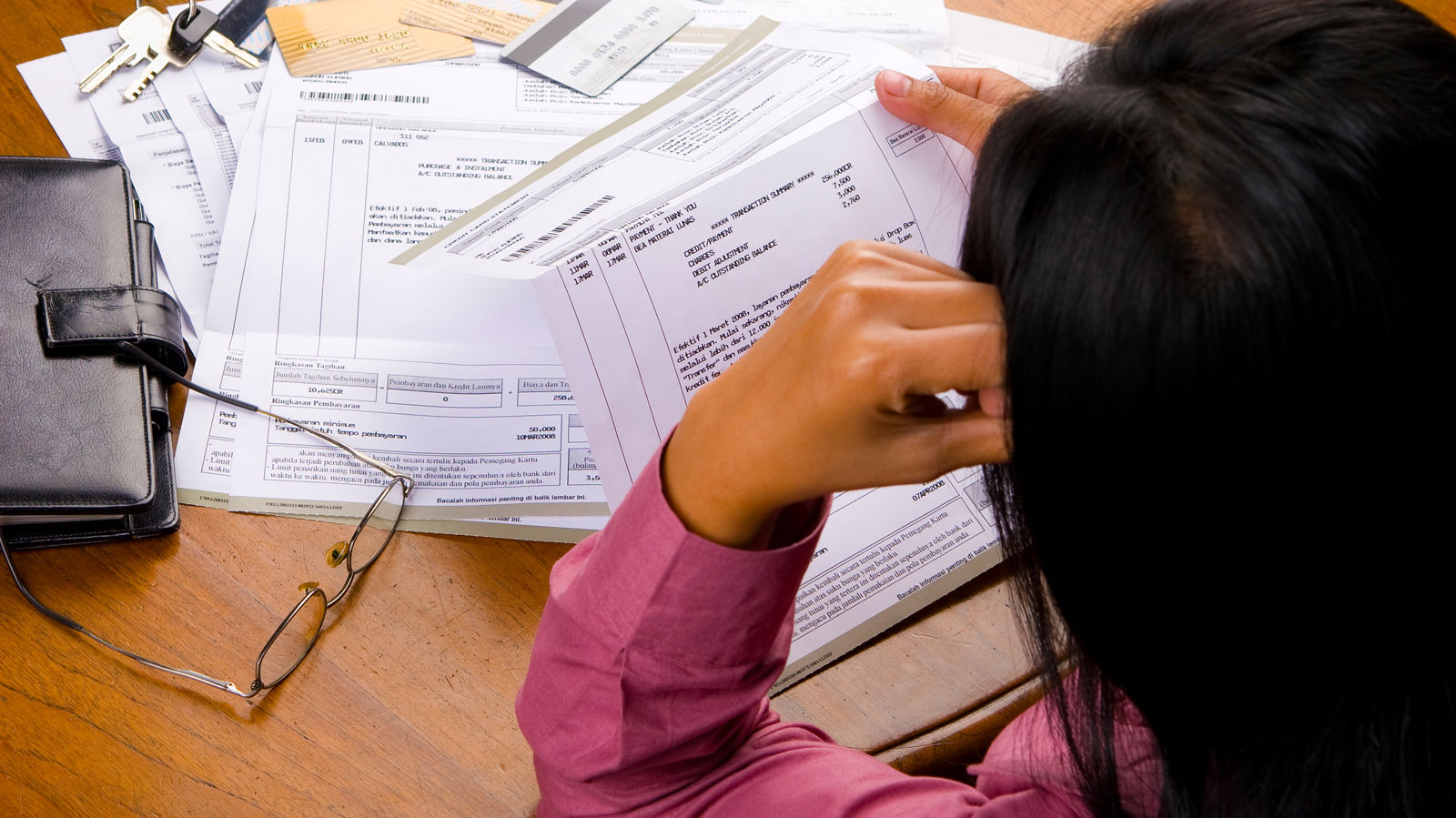

Mistakes on your credit report can cause a whole host of problems.

One of the most common complaints to the Consumer Financial Protection Bureau (CFPB) every year involves incorrect information on people’s credit reports.

Credit report errors are not unusual. A recent investigation by Consumer Reports found that one in three Americans who participated in the study discovered at least one mistake on their credit report. About 29 percent found mistakes in their personal information, while 11 percent discovered erroneous information about accounts.

Incorrect personal information can affect your ability to access your credit report or get your identity confirmed with government agencies if, for example, you’re trying to file an income tax return or access your Social Security account online.

Errors involving accounts or public records can hurt your ability to qualify for a loan or credit card, can increase the interest rates you pay or affect your premiums on auto or homeowners’ insurance policies.

Mistakes involving public records can also affect lending decisions and could potentially cost you a job offer if, for example, your credit report shows a bankruptcy or tax lien that isn’t yours.

You should go to AnnualCreditReport.com and you can request all three reports there – from Equifax, TransUnion and Experian. Or you can call 1-877-322-8228.

You will have to provide personal information including your Social Security number. For the rest of 2023, you can get a free credit report every week from each of the three bureaus. This was started in 2020 under COVID to help people learn whether payment extensions granted by banks were being honored or reported as late on credit reports. The free-report-a-week arrangement has been extended until Dec. 31, 2023. After that, you can request a copy from each bureau at no charge once a year.

IMPORTANT TIP: Do not go directly to the bureaus’ web sites; the reports won’t be free and you may mistakenly sign up for paid products, such as identity theft monitoring.

Your credit report may be a dozen pages or more. If you have never seen a copy of your credit report, or if it’s been a long time, here’s a roadmap of the places to look for the most common mistakes that will hurt you or could signal a problem.

Payment history. Do any of your current or past accounts show any late payments that weren’t late? This affects your credit score and potentially, lending decisions and interest rates.

Current balances. Credit scores depend significantly on the proportion of your credit limit you’re using. It’s best to have “credit in use” ratios of 25 percent or less. The balances are generally as of your last statement. You’re looking primarily for balances that seem way off or that you paid off long ago.

Inquiries. Your credit report will show “hard inquiries” involving actual applications for new loans or credit cards. And it will show “soft inquiries” or “account review” inquiries involving existing accounts. You should pay most attention to the hard inquiries: These affect your credit score. Are there inquiries on there you don’t recognize? And an erroneous inquiry could signal fraud.

Public records, such as lawsuits or liens. Public record entries hurt your credit score and your credit report. The entries usually come from court records: bankruptcies and civil suits seeking money owed. Credit reports used to show tax liens and judgments, but generally don’t any more, even if they exist. That could change in the future.

Consumer Watchdog, U.S. PIRG Education Fund

Teresa directs the Consumer Watchdog office, which looks out for consumers’ health, safety and financial security. Previously, she worked as a journalist covering consumer issues and personal finance for two decades for Ohio’s largest daily newspaper. She received dozens of state and national journalism awards, including Best Columnist in Ohio, a National Headliner Award for coverage of the 2008-09 financial crisis, and a journalism public service award for exposing improper billing practices by Verizon that affected 15 million customers nationwide. Teresa and her husband live in Greater Cleveland and have two sons. She enjoys biking, house projects and music, and serves on her church missions team and stewardship board.